Key Financials

On February 25, 2026, Salesforce reported Q4 FY26 (ending January 31, 2026) and full-year results. Marc Benioff used the word "incredible" 24 times during the earnings call — peak Benioff, but the numbers actually back it up.

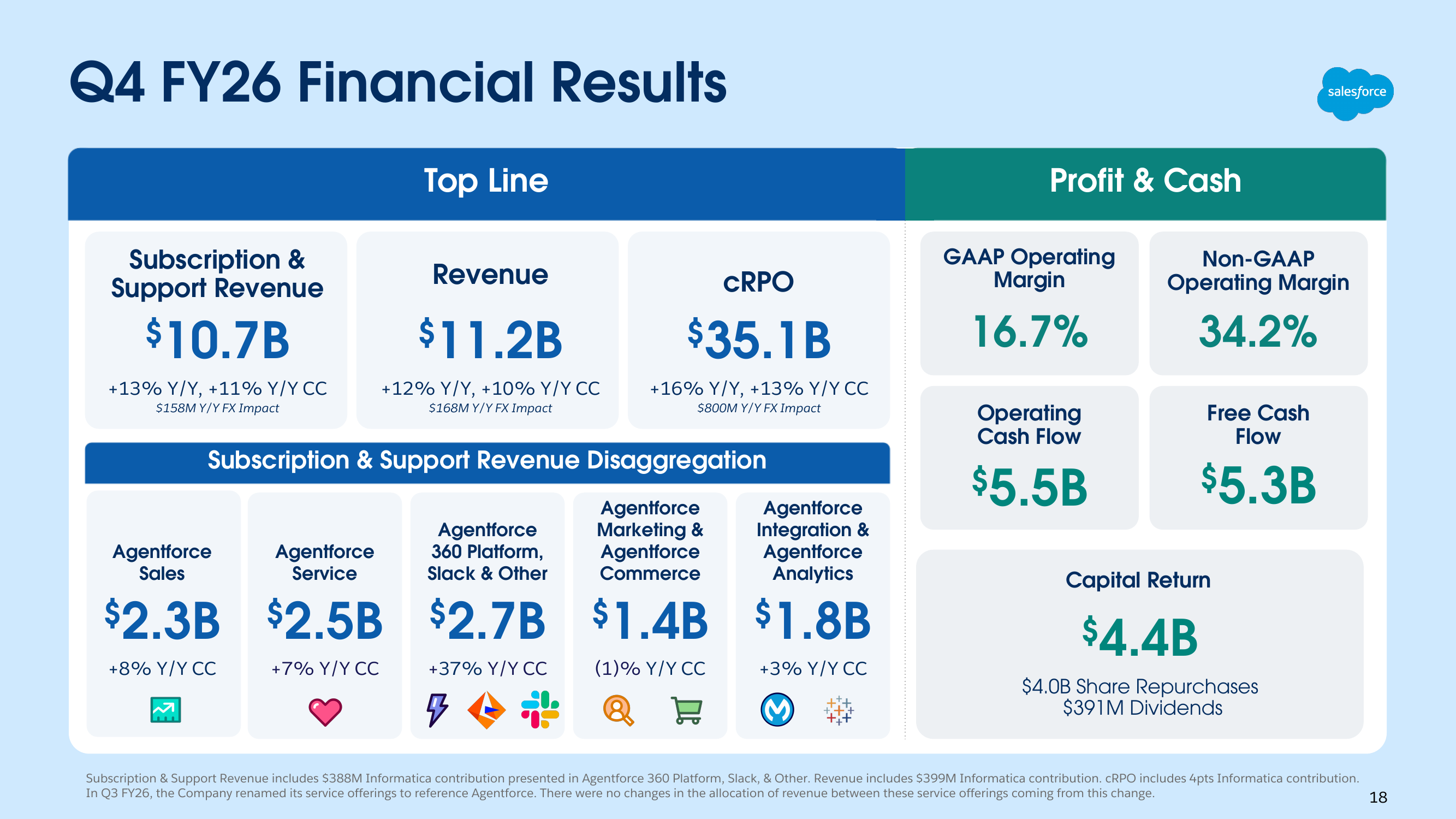

| Metric | Q4 FY26 | YoY Change |

|---|---|---|

| Revenue | $11.2B | +12% (incl. $399M Informatica contribution) |

| Subscription & Support | $10.7B | +13% (incl. $388M Informatica) |

| Non-GAAP EPS | $3.81 | Beat estimate by 24.9% (est. $3.05) |

| GAAP Operating Margin | Full year: 20.1% | |

| Non-GAAP Operating Margin | Full year: 34.1% | |

| Operating Cash Flow | Full year: $15.0B (+15%) | |

| Free Cash Flow | Full year: $14.4B (+16%) | |

| RPO | $72.4B | +14% |

| Current RPO | $35.1B | +16% |

Full-year revenue hit $41.5 billion, up 10% YoY, with organic growth around 9% (Informatica contributed approximately 3 percentage points). The EPS beat of nearly 25% was the standout. A 34.1% non-GAAP operating margin is top-tier for enterprise software — and Salesforce delivered it while still growing.

Benioff's money quote: "We've rebuilt Salesforce to become the operating system for the Agentic Enterprise, bringing humans and agents together on one trusted platform. And the more intelligence moves to where work happens, the more valuable Salesforce becomes."

The Agentforce Numbers: Unpacked

The most closely watched metrics all revolved around Agentforce:

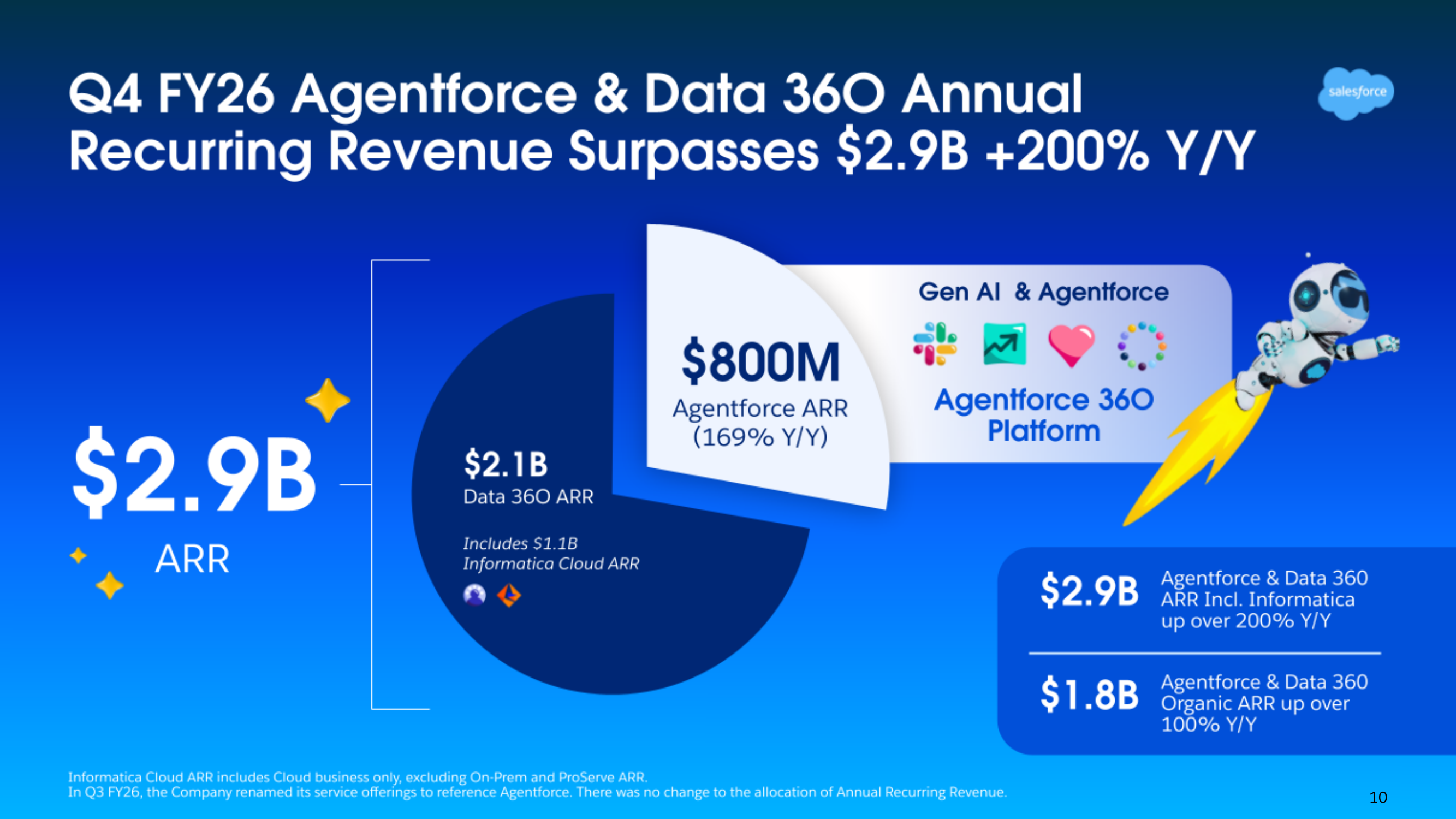

- Agentforce ARR: $800 million, up 169% YoY (up from $540M in Q3, a 48% sequential increase)

- Data 360 ARR: $2.1 billion, including $1.1B from Informatica Cloud

- Combined: $2.9 billion+, up over 200% YoY

- Organic combined (excluding Informatica): $1.8 billion, up over 100% YoY

- Deals closed: 29,000+, up 50% QoQ

- 75% of Q4's top 100 deals included both Agentforce and Data 360

- 12 deals over $10M in Q4, including 3 above $20M and 1 above $50M

A necessary note on data accounting: Salesforce reports Agentforce and Data 360 together at $2.9B ARR, but Data 360 includes $1.1B from Informatica Cloud — a company acquired for $8B in 2024. Strip that out, and organic ARR is $1.8B, still growing 100%+ YoY. That's strong, but meaningfully different from the "200%+ growth" headline. Investors should pay attention to this distinction.

That said, the 29,000+ deal count, 50% QoQ growth, and the fact that over 60% of Q4 bookings came from existing customer expansion — these signal genuine traction, not just land-grab. Twelve eight-figure deals (including one above $50M) show enterprise buyers are placing real bets.

Agentic Work Units: Salesforce's New Currency

This earnings report introduced a new metric: the Agentic Work Unit (AWU) — defined as "one discrete task accomplished by an AI agent: decisions made, records updated, workflows triggered, and more." Total AWUs delivered to date: 2.4 billion. Q4 alone produced 771 million (up 57% QoQ), powered by 19 trillion+ tokens (5x YoY).

The AWU growth curve is steep: from 14 million in Q1 FY25 to 771 million in Q4 FY26 — a 55x increase over eight quarters. The metric's value is that it measures actual usage rather than purchase intent — customers are genuinely putting agents to work. However, Salesforce has not published a precise definition of what constitutes one AWU. Is sending a single email one unit? Is a complex multi-step approval workflow also one unit? Without this clarity, external benchmarking remains difficult.

The "SaaSpocalypse" Narrative and Benioff's Rebuttal

The most viral moment from the earnings call was Benioff's pushback against the "SaaSpocalypse" narrative — the market thesis that AI agents will destroy traditional SaaS subscription models. His line: "We've all been reading about the SaaSpocalypse, but we've got our SaaSquatch that's eating it!" He followed up by noting this isn't his first market panic, citing 2008, 2016, 2020, and COVID.

Benioff's confidence rests on the $72B RPO figure — contracted revenue not yet recognized — up 14% YoY. This is not the backlog profile of a company being disrupted. He added a characteristically dry aside: "RPO does not matter, but evidently, we have it."

Valoir CEO Rebecca Wettemann offered a more measured take: Salesforce needs to demonstrate "how customers are moving AI agents from pilots to production at scale." The 29,000 deals are one thing; how many are running in production environments is a different and more important question.

The $50 Billion Buyback

Salesforce's Board authorized a new $50 billion share repurchase program (replacing all prior unused authorizations) and raised the quarterly dividend from $0.40 to $0.44 per share (+5.8%). In FY26, the company returned $14.3 billion to shareholders through $12.7B in buybacks and $1.6B in dividends — 99% of free cash flow.

A $50B buyback authorization is among the largest in tech. The signal is clear: management believes the stock is undervalued and backs the Agentforce growth story with capital allocation. For investors, this carries more weight than slide decks.

FY27 Guidance and the FY30 Target

| Metric | FY27 Guidance |

|---|---|

| Revenue | $45.8-46.2B (+10-11%, incl. ~3pts Informatica) |

| Organic Growth | ~7-8%, expected to accelerate in H2 |

| Subscription Revenue Growth | Slightly under 12% (incl. ~3pts Informatica) |

| Non-GAAP Operating Margin | 34.3% (continued expansion) |

| Non-GAAP EPS | $13.11-$13.19 |

| Operating Cash Flow Growth | ~9-10% |

| FY30 Revenue Target | $63B+ (incl. Informatica) |

The guidance subtlety: Wall Street expected $46.06B, and Salesforce guided to a $46.0B midpoint — nearly matching but slightly conservative. The market's immediate reaction was a 5%+ after-hours decline, which gradually recovered as investors digested the Agentforce metrics.

The $63B FY30 target (raised from the prior ex-Informatica basis) implies roughly 52% total growth over four years — about 11% annually. Not aggressive, but it requires Agentforce to scale meaningfully beyond its $800M ARR starting point. CFO Robin Washington signaled organic revenue re-acceleration in H2 FY27.

Signals for the Salesforce Ecosystem

This earnings report sends several clear signals to the Salesforce ecosystem:

First, Agentforce is no longer experimental — it's an $800M ARR business line. All of Q4's top 10 deals included Agentforce 360, Data 360, Agentforce Sales, Agentforce Service, Agentforce 360 Platform, and Agentforce Analytics. For SIs and ISVs, the roadmap must center on Agentforce.

Second, the Informatica integration has reached initial maturity, with Data 360 becoming Agentforce's data foundation. In FY26, Data 360 ingested 112 trillion records (+114% YoY), with 53 trillion via Zero Copy (+310% YoY). Data integration is no longer a standalone category — it's been redefined as infrastructure for the agent economy.

Third, industry verticalization is accelerating. Salesforce industry cloud ARR reached $6.6 billion (+20% YoY). The Q4 customer roster includes Amazon, AT&T, Ford, Siemens, Southwest Airlines, Wyndham Hotels, SharkNinja, Live Nation, MrBeast, Lennar, and Bouygues Telecom — spanning retail, telecom, automotive, industrial, aviation, hospitality, consumer electronics, entertainment, real estate, and communications.