$41.5 Billion: Unpacking Salesforce's FY2026 Report Card

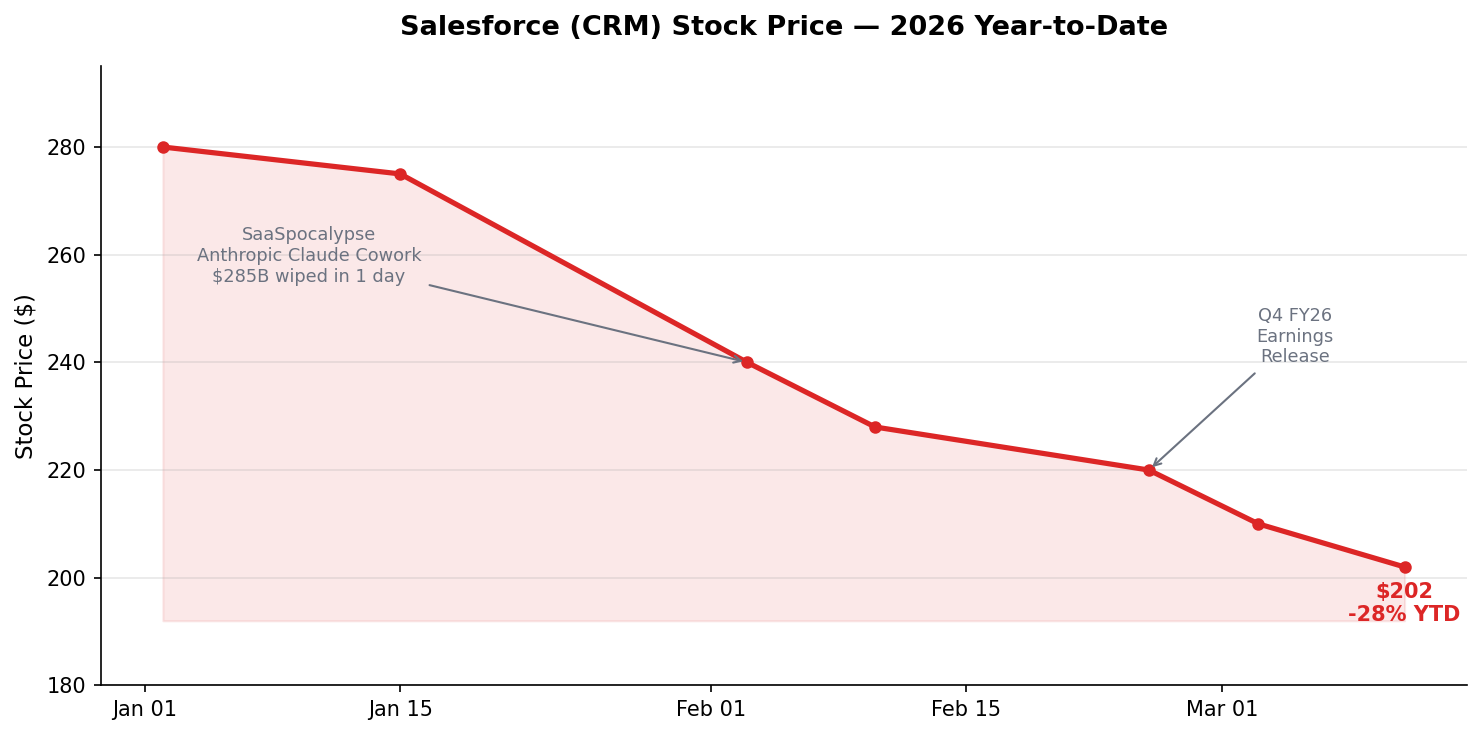

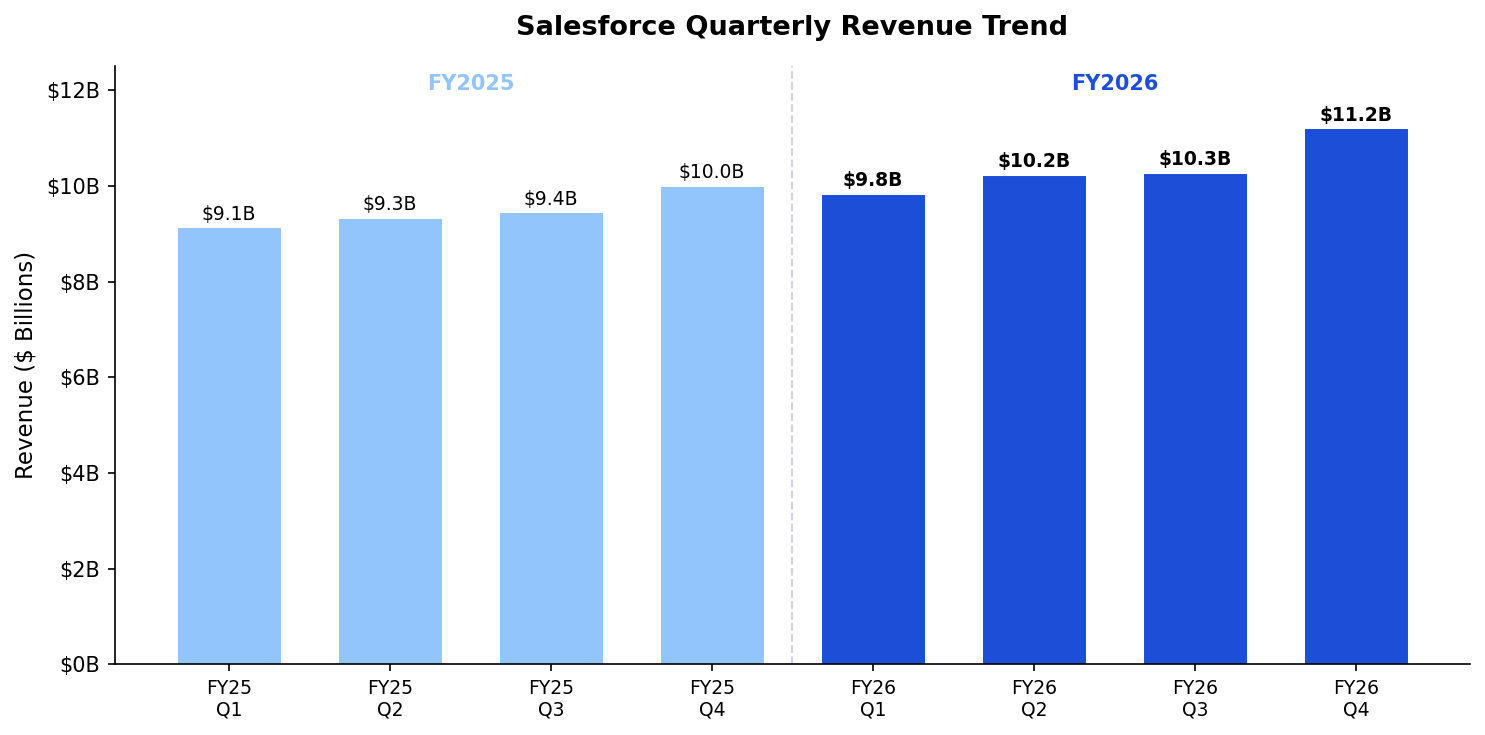

On February 25, 2026, Salesforce (NYSE: CRM) reported fourth-quarter and full-year results for fiscal year 2026 (ending January 31, 2026). Full-year revenue came in at $41.525 billion, up 10% year-over-year (9% in constant currency), including roughly $399 million from the Informatica acquisition. Q4 revenue was $11.201 billion, up 12% YoY — a new quarterly record.

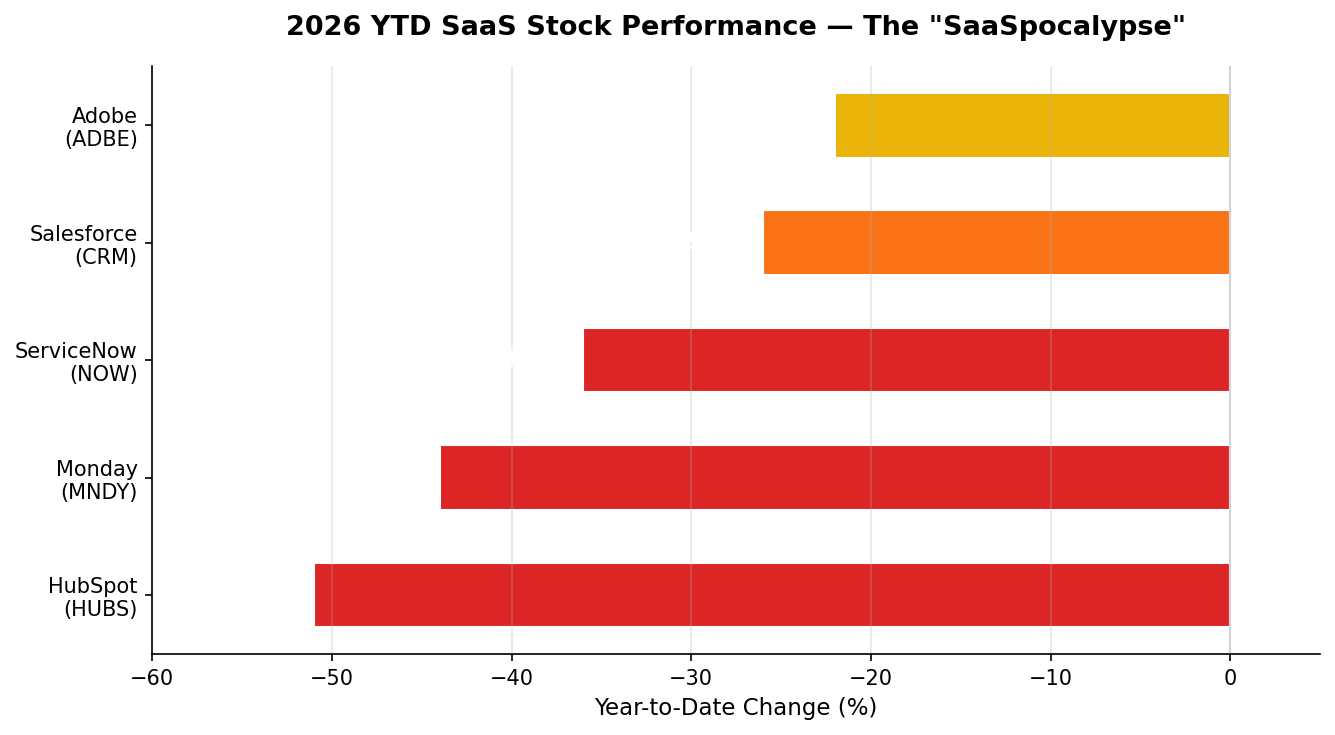

But this otherwise solid report card landed at possibly the worst timing imaginable. In early February 2026, the entire SaaS sector had just experienced what traders at Jefferies dubbed the "SaaSpocalypse" — an epic selloff triggered when Anthropic unveiled its Claude Cowork legal automation tool, vaporizing approximately $285 billion in enterprise software market cap in a single day. Within 30 days, nearly $2 trillion in SaaS market cap evaporated. Salesforce's stock is down more than 26% year-to-date.

Wall Street's fear is straightforward: if 10 AI agents can replace the work of 100 sales reps, you don't need 100 Salesforce seats anymore. The per-seat pricing model that underpinned the entire SaaS industry is under existential threat. In many ways, this earnings report was Salesforce's answer to that question — is Agentforce cannibalizing its own revenue, or opening up new growth?

All Five Business Lines Rebranded: Agentforce Is No Longer an Add-On

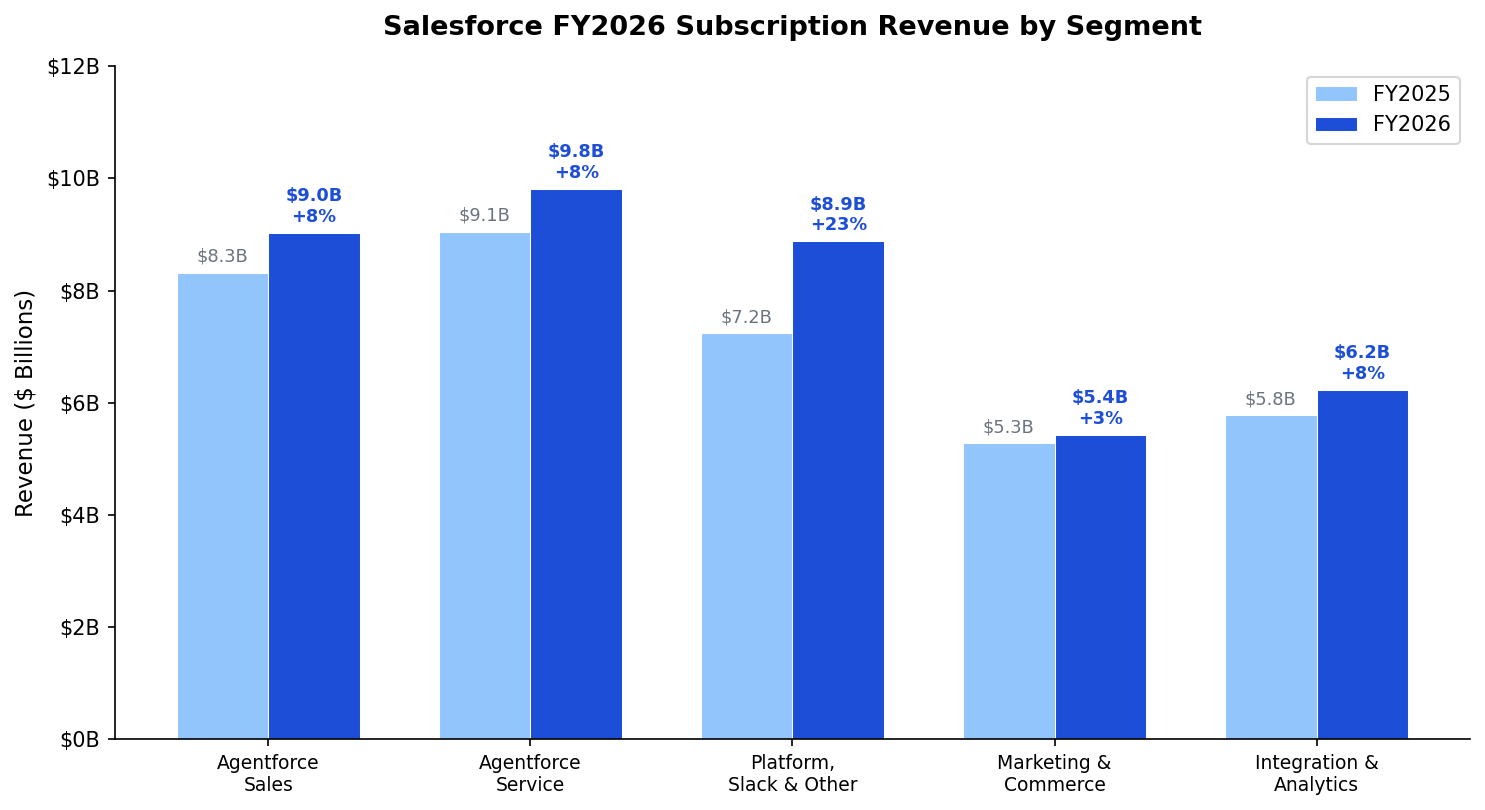

Starting Q3 FY26, Salesforce added the Agentforce prefix to every subscription service line. This move says a lot on its own — when you rebrand your company's primary revenue streams under a new name, you're either deeply confident in that brand or making a very large bet.

| Business Line (New Name) | FY2026 | FY2025 | YoY | Q4 CC Growth |

|---|---|---|---|---|

| Agentforce Sales (formerly Sales Cloud) | $9.028B | $8.322B | +8% | +8% |

| Agentforce Service (formerly Service Cloud) | $9.818B | $9.054B | +8% | +7% |

| Agentforce 360 Platform, Slack & Other | $8.882B | $7.247B | +23% | +37% |

| Agentforce Marketing & Commerce | $5.428B | $5.281B | +3% | (1)% |

| Agentforce Integration & Analytics | $6.232B | $5.775B | +8% | +3% |

| Total Subscription & Support | $39.388B | $35.679B | +10% | +11% |

Several things worth unpacking behind these numbers:

Where does Platform's 37% Q4 growth come from? Informatica contributed $388M for the full year, but even stripping out its Q4 contribution (roughly $150-200M), organic platform growth was still north of 20%. Slack and platform consumption revenue are the main drivers, and much of Agentforce's consumption-based billing flows through this segment.

Marketing & Commerce posted negative Q4 growth at (1)% in constant currency. The only business line to shrink. Marketing Cloud faces intensifying competition from HubSpot and Adobe, while Commerce Cloud is feeling macroeconomic consumer softness. At 3% full-year growth, this segment is clearly the weakest link.

Sales Cloud and Service Cloud are both steady at ~8%. These two "cash cow" segments account for nearly half of total subscription revenue. Their growth is neither exciting nor alarming — but that's exactly what bears worry about. If AI agents are truly replacing human seats at scale, why haven't these two largest segments shown any acceleration?

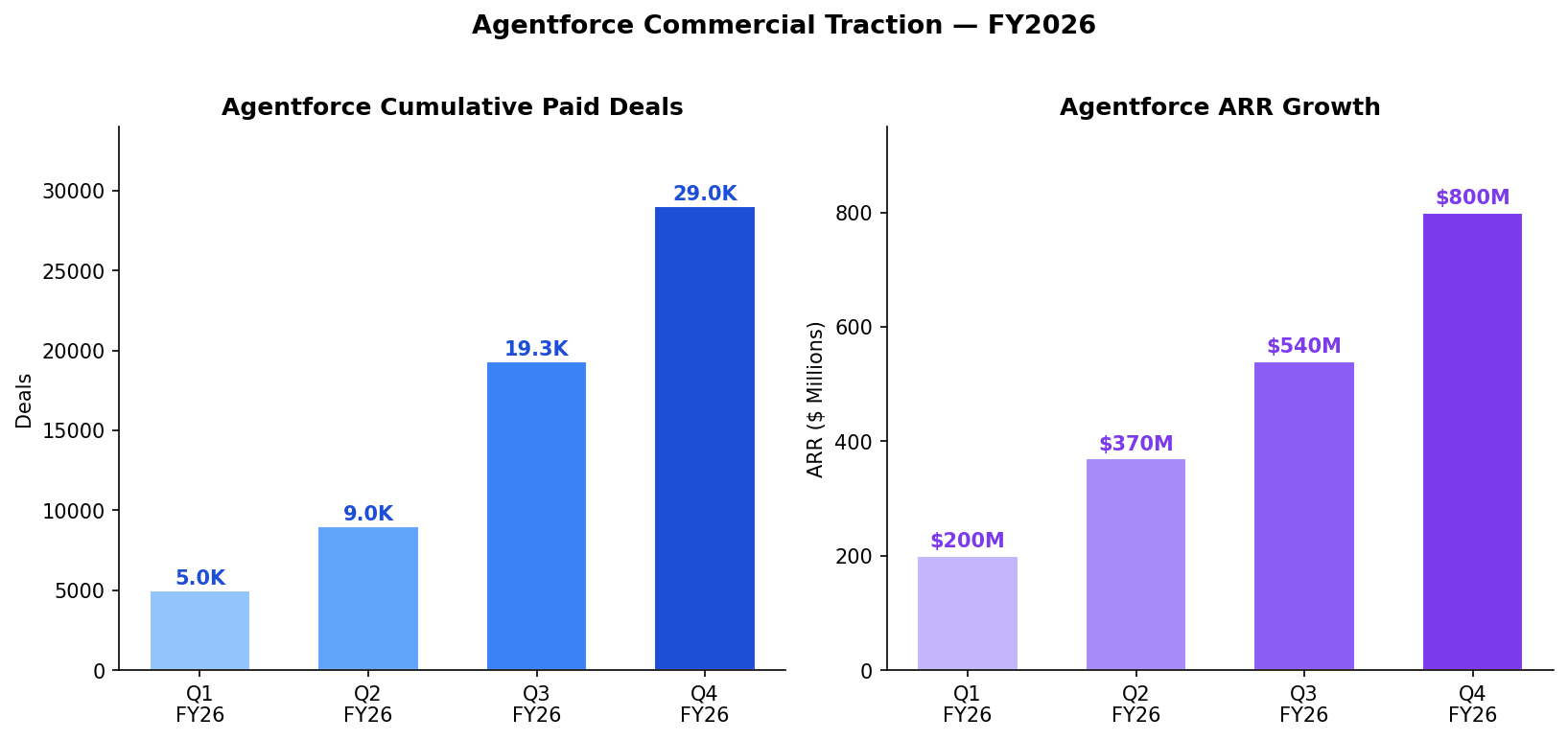

Agentforce Monetization: What $800M ARR Really Means

The core Agentforce metrics:

- ARR hit $800M, up 169% YoY (was $540M in Q3 — a 48% sequential jump)

- 29,000 cumulative paid deals, up 50% QoQ

- Production accounts grew nearly 50% QoQ

- Over 60% of Q4 Agentforce and Data 360 bookings came from existing customer expansion (upsell)

- Bookings for Agentforce 1 Edition and Agentforce for Apps (A4X) — the two most premium SKUs — nearly tripled QoQ

$800M ARR against $41.5B in total revenue is less than 2%. But the growth trajectory matters. If you naively extrapolate the Q3-to-Q4 sequential growth rate (48%), Agentforce ARR could approach $2.0-2.5B by end of FY27. That's before factoring in Data 360 and Informatica Cloud synergies.

Three Customer Stories Reveal Agentforce's Real-World Landing

On the earnings call, Salesforce brought in three customers whose stories illustrate Agentforce's positioning more clearly than the financial data alone:

Wyndham Hotels & Resorts: Deployed over 5,000 Agentforce instances across its 8,300+ hotels — and they're "just getting started." For a chain of this scale, the traditional model required multiple CRM seats per property. In an agent model, repetitive customer service tasks, booking management, and complaint resolution shift to AI agents, freeing human staff for higher-value work.

SaaStr (Jason Lemkin's SaaS community): Went from 15 humans to 2.5 humans + 20 agents. Closed $2.7M in revenue via Agentforce with another $3.5M in pipeline. This case directly addresses the "will AI reduce seats" fear — yes, it does. Salesforce's play is to replace lost seat revenue with consumption-based billing (charging by agent work completed).

US Army: Awarded Salesforce a 10-year IDIQ contract with a $5.6 billion ceiling. This isn't just an Agentforce win — it's a landmark government vertical deal. A $5.6B contract ceiling means massive long-term revenue lock-in.

AWU: A New Billing Unit Taking Shape

Salesforce formally introduced Agentic Work Units (AWUs) as a metric this quarter. To date, the Agentforce platform has delivered 2.4 billion AWUs (up 57% QoQ), consuming nearly 20 trillion tokens (up 5x YoY).

AWU matters because it's likely the foundation for Salesforce's next-generation pricing model. Traditional SaaS charges per seat. Agentforce charges per outcome — per AWU. As Benioff said on the call: "AI wasn't just reasoning — it was delivering real work." The implication is clear: you're paying for actual work delivered, not a vague AI promise.

Data 360 and Informatica: The Data Foundation Story

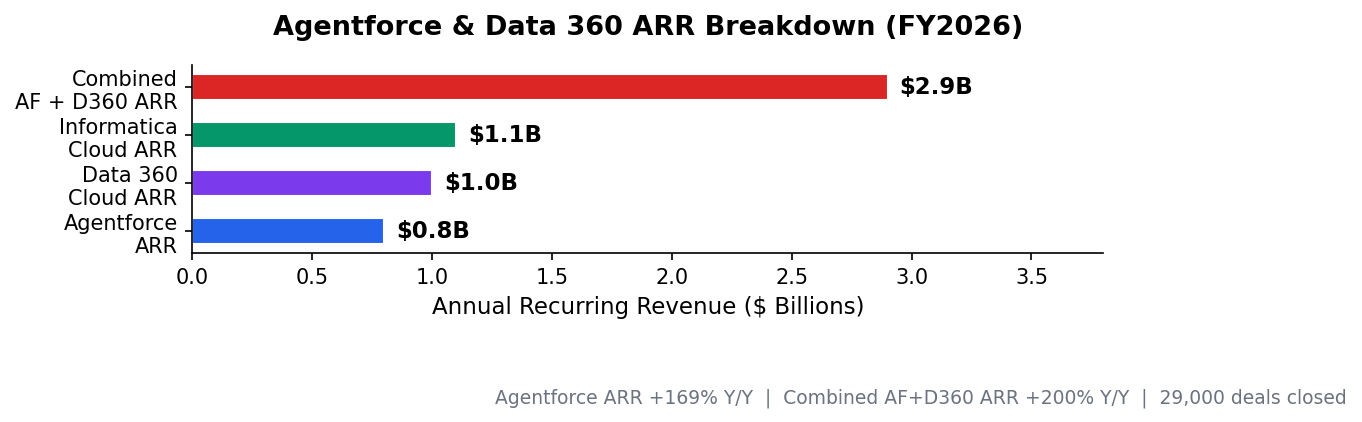

Combined Agentforce + Data 360 ARR exceeded $2.9B (up 200%+ YoY), broken down as follows:

- Agentforce ARR: $800M (+169% YoY)

- Data 360 Cloud ARR: ~$1.0B

- Informatica Cloud ARR: $1.1B

Data 360 (formerly Data Cloud) ingested 112 trillion records in FY2026, up 114% YoY. Zero Copy ingestion reached 53 trillion records (+310% YoY), and 18 terabytes of unstructured data were processed. These data volumes are the foundation for Agentforce's RAG (Retrieval Augmented Generation) and grounding capabilities — agent response quality is directly tied to the quality and breadth of the underlying data.

The Informatica acquisition closed in Q3 FY26 (November 2025) for approximately $8 billion. The balance sheet impact is clear: goodwill jumped from $51.283B to $57.941B (+$6.658B), intangible assets from $4.428B to $6.815B, and long-term debt from $8.433B to $10.439B — Salesforce issued $6 billion in new debt to finance the deal.

What does Informatica bring? Core ETL/ELT capabilities, master data management (MDM), and data governance. Benioff has called the acquisition "transformational" on multiple occasions. Data 360 + MuleSoft + Informatica create a complete pipeline from data ingestion through governance to data services. For Agentforce, this means agents can access broader, cleaner enterprise data sources.

Profitability, Cash Flow, and Capital Returns

| Metric | Q4 FY26 | Q4 FY25 | FY26 | FY25 |

|---|---|---|---|---|

| Total Revenue | $11.201B | $9.993B | $41.525B | $37.895B |

| Gross Margin | 78% | 78% | 78% | 77% |

| GAAP Operating Income | $1.869B | $1.820B | $8.331B | $7.205B |

| GAAP Operating Margin | 16.7% | 18.2% | 20.1% | 19.0% |

| Non-GAAP Operating Margin | 34.2% | 33.1% | 34.1% | 33.0% |

| GAAP Net Income | $1.943B | $1.708B | $7.457B | $6.197B |

| Non-GAAP Diluted EPS | $3.81 | $2.78 | $12.52 | $10.20 |

| Operating Cash Flow | $5.464B | $3.970B | $14.996B | $13.092B |

| Free Cash Flow | $5.323B | $3.816B | $14.402B | $12.434B |

A few things worth digging into:

Why was Q4 GAAP operating margin 3.4 percentage points below the full-year figure? Two main factors: sales and marketing expenses hit $4.017B (36% of revenue), up 16% YoY as Salesforce poured resources into AI go-to-market; and restructuring charges of $286M, though down slightly from $298M a year ago, still weighed on margins.

How did Non-GAAP EPS blow past estimates by 25%? Wall Street expected $3.05; actual was $3.81. Much of the upside came from strategic investment gains of $811M in Q4 (versus just $96M a year ago), contributing roughly $0.66/share. Strip out that one-time item and the core beat was solid but less dramatic.

$14.4B in free cash flow, $12.7B in buybacks. Salesforce plowed 88% of its free cash flow into stock repurchases. Add $1.6B in dividends, and total shareholder returns of $14.3B nearly consumed the entire free cash flow. The board then authorized a fresh $50 billion buyback program — roughly 20% of the current market cap. Is this supreme confidence, or a hedge against decelerating growth?

Balance Sheet Changes

Informatica reshaped the balance sheet significantly:

| Balance Sheet Item | Jan 31, 2026 | Jan 31, 2025 | Change |

|---|---|---|---|

| Cash & Equivalents | $7.327B | $8.848B | -17% |

| Accounts Receivable | $14.339B | $11.945B | +20% |

| Goodwill | $57.941B | $51.283B | +$6.658B |

| Total Assets | $112.305B | $102.928B | +9% |

| Unearned Revenue | $24.317B | $20.743B | +17% |

| Noncurrent Debt | $10.439B | $8.433B | +24% |

| RPO (Remaining Performance Obligation) | $72.4B | $63.4B | +14% |

RPO at $72.4 billion is a key forward-looking indicator — it represents contracted revenue not yet recognized. Of that, $35.1B is current RPO (recognized within 12 months), up 16% YoY. RPO growth (14%) outpacing revenue growth (10%) means deal signings are running ahead of delivery — a positive signal.

FY2027 Guidance: Has Growth Peaked?

| FY2027 Metric | GAAP | Non-GAAP |

|---|---|---|

| Full-Year Revenue | $45.8–46.2B | +10-11% CC, incl. ~3pp Informatica |

| Q1 Revenue | $11.03–11.08B | +10-11% CC |

| Subscription Revenue Growth | Slightly under 12% | ~11% CC |

| Operating Margin | 20.9% | 34.3% |

| Diluted EPS | $7.85–$7.93 | $13.11–$13.19 |

| Operating Cash Flow Growth | ~9-10% | — |

| Free Cash Flow Growth | — | ~9-10% |

Strip out Informatica's ~3 percentage point contribution, and FY27 organic revenue growth sits at roughly 7-8% — essentially flat versus FY26. Management offered an important qualitative promise: organic revenue will "re-accelerate in H2 FY27." CFO Robin Washington was explicit on this point, but provided no specific numbers.

Wall Street split into two camps:

The bulls (Morgan Stanley, Deutsche Bank, Barclays) argue Agentforce is still in "early innings," with 29,000 deals barely scratching the surface. Morgan Stanley analysts cited partner feedback indicating "we are in the very early stages." Deutsche Bank maintains a buy rating with a $255 target (lowered from $325). Barclays carries an overweight rating implying 38% upside.

The bears (Bernstein, UBS) take a sharper view. Bernstein's Mark Moerdler sees "limited upside and meaningful downside risk," rating the stock underperform. UBS analyst Karl Keirstead points out the issue isn't Agentforce itself — that product looks genuinely promising — it's the overwhelming majority of Salesforce's revenue that comes from legacy products (Sales Cloud, Service Cloud) where seat-based growth is flatlining. Can new Agentforce revenue offset potential seat erosion in the core business?

Salesforce's own answer: a raised FY2030 revenue target of $63 billion (including Informatica), implying ~11% CAGR from FY26 through FY30. And Benioff directly addressed the "SaaSpocalypse" narrative on the call with trademark defiance: "This isn't our first SaaSpocalypse." His message: we survived the dot-com bust, the 2008 financial crisis, and the 2020 pandemic. We'll survive this too.

Regional Revenue and Industry Verticals

| Region | FY2026 | FY2025 | YoY | Q4 CC Growth |

|---|---|---|---|---|

| Americas | $27.193B | $25.143B | +8% | +9% |

| Europe | $10.017B | $8.891B | +13% | +13% |

| Asia Pacific | $4.315B | $3.861B | +12% | +13% |

Europe and Asia Pacific growing at 13% significantly outpaced the Americas at 9%. Two implications: first, Salesforce still has substantial penetration headroom in international markets; second, AI agent adoption isn't just a US story — global enterprises are following fast.

On industry verticals, Salesforce disclosed that its industry-specific businesses finished the year at $6.6 billion ARR, up roughly 20% YoY. This spans financial services, healthcare, retail and consumer goods, manufacturing, and other vertical-specific solutions. Vertical growth outpacing the company average suggests the Industry Cloud strategy is paying off.

What This Means for the Salesforce Ecosystem

For Salesforce admins and developers, this report sends several clear signals:

1. Agentforce proficiency has gone from "nice to have" to "table stakes." With 29,000 paid contracts, customers are actively deploying agents. If you haven't built anything in Agentforce Builder yet, now's the time. The agent evaluation framework and Spring '26 production playbook are practical starting points.

2. Consumption-based pricing is becoming the new normal. The AWU metric wasn't introduced casually — it points directly to a shift from per-seat to per-outcome pricing. SaaStr's case (15 humans to 2.5 humans + 20 agents) is a preview of this transition. Admins need to understand Agentforce billing models, token consumption patterns, and AWU cost structures.

3. Data 360 + Informatica means the data layer is leveling up. 112 trillion records ingested, Zero Copy, unstructured data processing — these capabilities will increasingly surface in everyday admin and developer tools. Spring '26 already integrates Data Cloud features into Setup and Flow.

4. The "Agentforce-ification" of Sales and Service Cloud is the mega-trend. Rebranding product lines isn't just a marketing exercise. Technically, every cloud is embedding agent capabilities. Sales Cloud's Einstein Copilot has evolved into Agentforce Sales Agent; Service Cloud agents can now autonomously resolve customer inquiries. Developers should track the MCP protocol and agent orchestration capabilities.

5. Traditional skills aren't going away. $39.3 billion in subscription revenue still overwhelmingly comes from traditional CRM functions — sales management, service tickets, marketing automation, integration development. Agentforce is incremental, not a replacement. The most valuable professionals in the market will be those who combine traditional Salesforce administration with agent configuration expertise.